MSME

Registered

Wedline

Registered

We Deliver

Clutch

28+ Reviews

250+ Projects

Completed

125+ Happy

Clients

MSME

Registered

Wedline

Registered

We Deliver

Clutch

28+ Reviews

250+ Projects

Completed

125+ Happy

Clients

Date: 29-04-2026

By BM Coder — Enterprise Software Development Company

Every modern fintech product is actually a network of systems pretending to be one product. Your mobile app talks to a payment gateway. That gateway talks to a card network. Your onboarding flow calls a KYC vendor, a PAN verification API, an Aadhaar vault, and a fraud scoring engine. Meanwhile, accounting needs the same transaction in Tally or Zoho, support needs it in Freshdesk, and leadership needs it in Power BI.

Without integration, each system becomes an island. Teams export CSVs, build manual reconciliations, and chase data mismatches at month end. The cost is not just engineering hours. It is slow onboarding, failed payments, compliance risk, and customers who leave because the experience feels broken.

API integration is how you connect those islands. Done right, it creates a single, reliable flow of data across your entire stack, in real time, with security and auditability built in. At BM Coder, we design these flows every day for banks, NBFCs, payment companies, wealth platforms, and insurance startups. Our software development for fintech practice focuses specifically on building API-first architectures that scale from first 1,000 users to 10 million transactions a day.

BM Coder builds secure, compliant integrations for payments, lending, KYC, core banking, and accounting. Talk to our architects today.

Email: [email protected]

WhatsApp: +91 95869 79730

An API, or Application Programming Interface, is a contract. It defines how one system can ask another for data or to perform an action, without needing to know how that other system works internally. Integration is the engineering work to make those contracts reliable in production.

It is more than just calling an endpoint. Production grade integration includes authentication, error handling, retries with exponential backoff, idempotency, data mapping, versioning, observability, and compliance logging. When you connect a loan origination system to a bureau like CIBIL, or a wallet to UPI, you are not just moving JSON. You are moving money, identity, and risk. The integration must be correct every single time.

Seamless data flow happens when these contracts are composed into pipelines. A customer completes eKYC. That event triggers a webhook. Your backend validates the payload, enriches it with risk data, writes to your core database, pushes to your CRM, and emits an event to your analytics warehouse. All of this happens in under two seconds, with no human in the loop.

Most fintech integrations share the same building blocks. First, identity and auth, typically OAuth 2.0 client credentials, mTLS, or signed JWTs. Second, the transport, usually HTTPS for request response, and webhooks or message queues for events. Third, the schema, which defines fields, types, and validation rules. Fourth, the lifecycle controls, like rate limits, circuit breakers, and dead letter queues.

Choosing the right API style matters early. REST remains the default for its simplicity and tooling. GraphQL is powerful when frontends need flexible data shapes. gRPC excels for low latency internal services. Webhooks are essential for real time notifications. Event streaming with Kafka or Redpanda is the foundation for ledger updates and fraud detection at scale.

| API Style | Best For | Key Strengths | Watch Outs |

|---|---|---|---|

| REST | Payments, KYC, account opening | Wide adoption, caching, simple debugging | Over fetching, multiple round trips |

| GraphQL | Mobile apps, dashboards | Single request for complex data, strong typing | Complexity in caching and rate limiting |

| gRPC | Internal microservices, pricing engines | High performance, protobuf contracts | Harder for third parties, needs HTTP2 |

| Webhooks | Payment status, mandate updates, disputes | Real time push, reduces polling | Requires signature verification and replay handling |

| Event Streaming | Ledger, fraud, analytics | Durable, ordered, replayable streams | Operational overhead, schema governance |

In fintech, data flow equals money flow. A delay of 500 milliseconds in a payment confirmation can create a duplicate charge. A missing webhook can leave a loan in pending state, blocking disbursal. An inconsistent customer ID across KYC and core banking can trigger a compliance audit.

Our fintech software development services solve this by treating integration as a product capability, not a one off script. We implement a canonical data model for customer, account, transaction, and ledger. Every external API is mapped into this model through an anti corruption layer. This means if you switch from one KYC vendor to another, your downstream systems do not break.

Seamless flow also unlocks growth. With clean APIs, you can launch UPI AutoPay in two weeks instead of two months. You can embed lending offers inside a partner app. You can reconcile all settlements automatically and close books daily instead of on day 10.

We have delivered more than 80 integrations across the fintech stack. The patterns repeat, but the stakes change.

For digital payments, we connect apps to Razorpay, Cashfree, Stripe, and directly to NPCI rails. The flow includes creating an order, handling redirects, verifying webhook signatures, updating transaction state with idempotency keys, and reconciling settlements against bank statements.

For onboarding and KYC, we orchestrate PAN verification, Aadhaar XML or Digilocker, face match, liveness, and PEP sanctions screening. Each vendor has different SLAs and error codes. We normalize them into a single KYC status machine with clear retry and manual review paths.

For lending, we integrate with bureaus, bank statement analyzers, account aggregators under the AA framework, eNACH, and eSign providers. The critical piece is data consistency across the loan management system, collections, and accounting.

For core operations, we sync with CRMs, ERPs, support desks, and data warehouses. This is where most data leaks happen. We use event driven CDC pipelines so that every transaction appears in analytics within seconds, not hours.

| System Pair | Integration Goal | Data Flow | Measured Impact |

|---|---|---|---|

| App to Payment Gateway | Instant confirmation | Order create, webhook verify, status update | 40 percent fewer support tickets for payment status |

| KYC Stack to Core | Faster onboarding | Normalized KYC result, risk score, document vault link | Onboarding time from 8 minutes to 2.3 minutes |

| LMS to Account Aggregator | Better underwriting | Consent, fetch, categorization, score | 15 percent improvement in approval rates |

| Core Banking to ERP | Automated reconciliation | Journal entries, settlement files, GST mapping | Daily close, zero manual entries |

| Transactions to Warehouse | Real time analytics | CDC stream, transformation, modeling | Fraud alerts within 30 seconds |

Early stage startups often start with direct point to point calls. It works for the first three vendors. At ten vendors, it becomes a mesh of brittle dependencies. Any change breaks multiple flows.

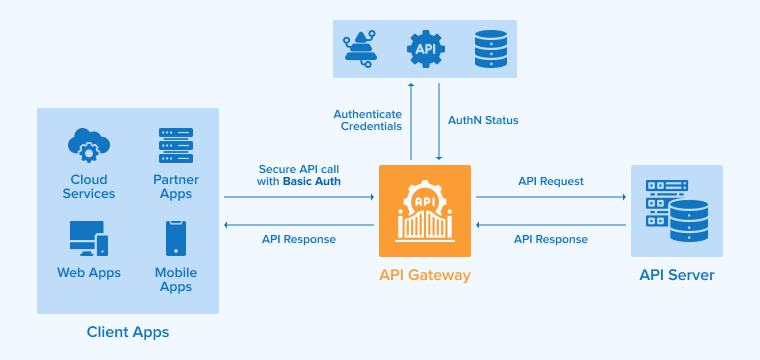

We recommend an API led approach. An Experience API serves your app and partners. A Process API orchestrates business logic like payment processing or loan approval. A System API wraps each external vendor with a stable contract. All traffic goes through an API gateway for auth, rate limiting, and observability.

This pattern gives you three wins. First, you can swap vendors without rewriting business logic. Second, you get centralized security and audit logs for RBI or PCI audits. Third, you can scale teams because frontend, backend, and integrations evolve independently.

Fintech integrations are regulated workloads. You cannot treat security as an afterthought. Every integration we build at BM Coder includes mTLS or OAuth 2.0, request signing, encrypted secrets management, PII tokenization, and detailed audit trails.

For India, we align with RBI guidelines on data localization, PA PG guidelines, and the Digital Personal Data Protection Act. For global clients, we map to PCI DSS for card data, SOC 2 for controls, and GDPR for consent. Webhook endpoints are always verified with HMAC signatures, replay protected with timestamps, and idempotent.

We also implement data minimization. Your analytics warehouse does not need full PAN numbers. It needs a token. Your support desk does not need full card numbers. It needs last four digits. These choices reduce blast radius and simplify audits.

Seamless does not mean slow. We design for p95 latency under 300 ms for synchronous APIs and end to end processing under 2 seconds for critical flows. Key techniques include connection pooling, async workers for webhooks, outbox pattern for guaranteed delivery, and sagas for distributed transactions.

Idempotency is mandatory. Every payment or payout request carries an idempotency key stored for at least 24 hours. Retries use jittered exponential backoff. Circuit breakers prevent cascading failures when a vendor degrades. Dead letter queues ensure no event is lost.

| Level | Characteristics | Risks | Next Step |

|---|---|---|---|

| 1. Ad Hoc | Direct calls, hardcoded keys, manual CSVs | Outages, data loss, audit failures | Introduce gateway and secrets manager |

| 2. Standardized | Central auth, logging, retry policies | Vendor lock in, slow changes | Build system APIs and canonical model |

| 3. Orchestrated | Process APIs, event driven flows | Observability gaps | Add tracing, metrics, alerting |

| 4. Platform | Self service APIs, developer portal, sandbox | Governance complexity | Automate compliance and cost controls |

First, treating webhooks as optional. Many teams poll for status. Polling fails under load and creates reconciliation gaps. We make webhooks the source of truth, with polling only as a fallback.

Second, no canonical model. Each team invents its own customer object. We define one model and enforce mapping at the system API boundary.

Third, weak error taxonomy. Vendors return hundreds of error codes. We normalize them into five categories, retryable, authentication, validation, business decline, and system error, and build playbooks for each.

Fourth, missing observability. You cannot fix what you cannot see. We add distributed tracing with correlation IDs, structured logs, and dashboards for success rate, latency, and reconciliation drift.

We use a proven framework for every integration project in our custom fintech development engagements.

This framework reduces integration time by 30 to 50 percent compared to ad hoc builds, while improving reliability and audit readiness.

Gateway: Kong or Apigee for policy enforcement. Service mesh: Istio for mTLS internally. Streaming: Kafka or Redpanda for events. Workflow: Temporal for durable orchestrations. Secrets: HashiCorp Vault. Observability: OpenTelemetry, Prometheus, Grafana, and ELK. Testing: Prism for contract testing, Postman and Karate for automation.

The stack matters less than the patterns. We choose tools that fit your cloud, team skills, and compliance perimeter, whether AWS Mumbai, GCP, or on premise.

Track four categories. Speed: time to onboard, time to first payment, lead time to add a new vendor. Reliability: API success rate, webhook delivery rate, reconciliation break rate. Cost: manual effort hours saved, infra cost per million calls. Risk: audit findings, PII exposure incidents, failed compliance checks.

A typical mid stage fintech sees onboarding drop from 7 minutes to under 3, payment success improve by 2 to 3 percent due to better retries, and finance close effort reduce by 80 percent after automated reconciliation. These gains compound every month.

India's Account Aggregator ecosystem, ONDC for financial services, and global open banking standards are making APIs the default distribution channel. The next wave is AI agents that act on APIs, for example an agent that negotiates a better loan rate by calling multiple lenders, or a treasury bot that sweeps balances based on real time cash flow.

These agents need the same foundations, strong contracts, idempotency, and observability. Companies that invest in API led connectivity today will be ready to expose safe, monetizable APIs to partners and agents tomorrow.

Features can be copied. Integrations cannot, because they embed your operational excellence, your compliance posture, and your data model into the way money moves. API integration is how you turn a collection of vendors into a coherent fintech platform that feels instant, reliable, and secure to customers.

BM Coder helps you get there faster. We architect, build, and operate the integration layer so your team can focus on product and growth.

Let's design your API integration roadmap. Get a free architecture review and a 2 week implementation plan for your highest impact flow, payments, KYC, or reconciliation.

Contact BM Coder

Email: [email protected]

WhatsApp: +91 95869 79730

We deliver software development for fintech across India, UAE, US, and UK.

Author: parth